Are You Accepting Credit Cards? Follow These 25 Best Practices (Infographic)

You and your customers enter into an agreement every time you accept a credit card – your customers agree that they won’t file a dispute if they receive the goods or services as expected, and you agree to be held liable for the amount if a chargeback or dispute over the transaction occurs.

A chargeback occurs when a credit card transaction is reversed by the issuing bank. Unlike refunds, you may incur a fee on top of the amount you have to pay back, and you probably won’t get the product back. The most common reasons for a chargeback are:

- the customer didn’t receive the service or product they purchased;

- the service or produce was not as advertised;

- the customer was charged the wrong amount or was charged twice;

- the customer didn’t recognize the charge on their statement; and

- fraud, either through identity theft or a customer using the credit card with the intent of requesting a chargeback later.

If you follow these credit card best practices, you’ll reduce your risk of receiving a chargeback, and you’ll be better prepared if you do get one.

Keyed-In and Online Payments

Keyed-in and online payments are risky because the customer doesn’t have to physically be there. When you accept keyed-in and online payments, take extra steps to protect yourself:

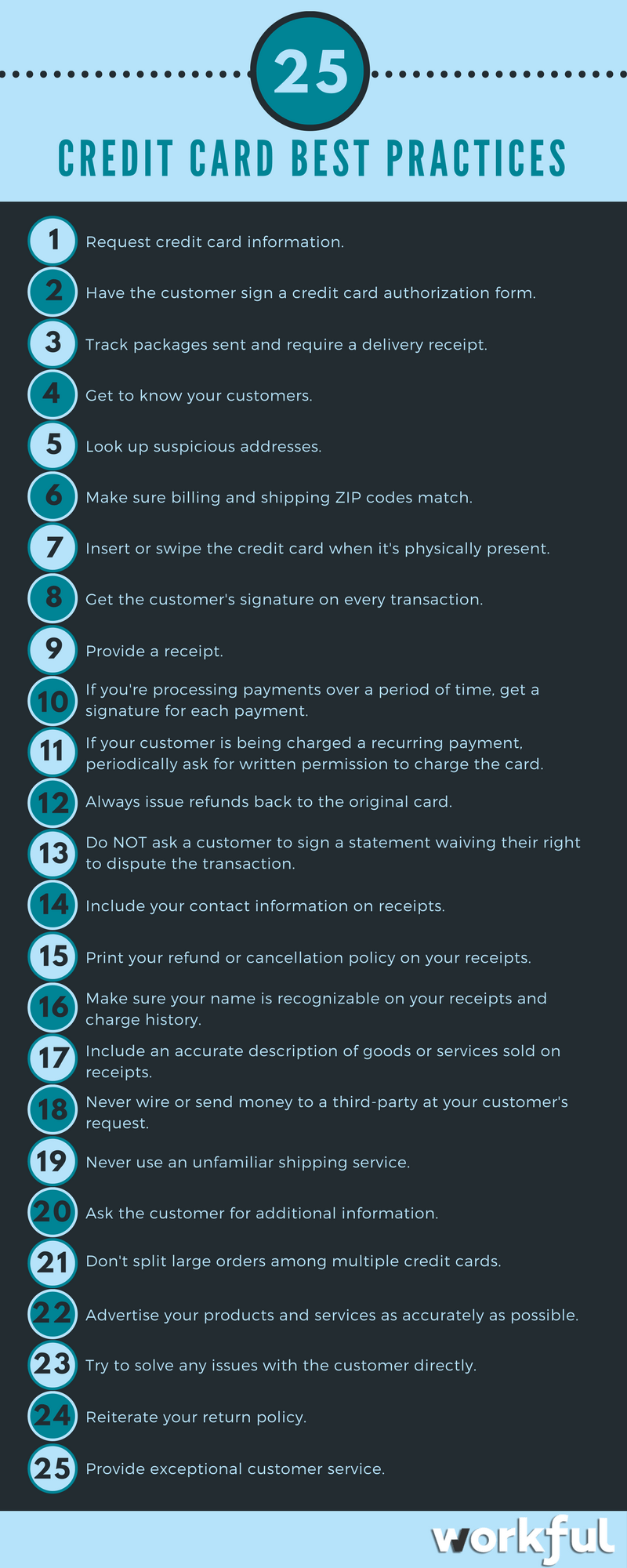

- Request the card information, like the cardholder’s name, billing address, card number, expiration date, and CVV code on the back of the credit card.

- Have the customer sign a form authorizing the payment and acknowledging that they understand your return policies. Keep this form on file, particularly if a customer is making a large purchase.

- If you’re shipping products to a customer, keep the tracking information and get a delivery receipt. If you’re sending a large or expensive item, require signature confirmation on delivery.

- Before you process large transactions, get to know your customers. Verify their company name and their billing address. You can do a Google search or even ask for a government ID – just make sure the name and address on the ID matches the name and billing address for the credit card.

- Look up suspicious addresses. Research the billing address and shipping address of orders that seem suspicious. You can use Google Maps or Zillow to help you determine their legitimacy.

- Compare billing and shipping ZIP codes. If you’re shipping products to a customer, make sure the shipping ZIP code is the same as the billing ZIP code. If they’re not the same, call the customer and ask them why. Accept the payment if their answer makes sense. Don’t accept their payment if they don’t have a reasonable explanation.

In-Person Payments

Swiping or inserting a credit card is safer than keying in a card, but there are still some best practices to follow to protect your business.

- If the card is physically present, always insert or swipe the card. You have a higher chance of winning a dispute on an inserted or swiped and signed payment than if you key in the information manually.

- Get a customer signature on every transaction. Doublecheck that the signature matches the signature on the back of the credit card. If the card isn’t signed, ask the customer for a government issued ID and to sign the back of the card. You can’t require that a customer show you their ID and seeing that ID won’t change your liability for the transactions, but an unsigned card is invalid and should not be accepted. So, if a customer with an unsigned card refuses to show you their ID, don’t accept their credit card.

- Provide a receipt. A receipt will remind the customer what they bought and can help represent you in the case of a dispute.

Processing Payments

When it comes to actually processing the payments or providing a return, there are some things you can do to protect yourself.

- If you’re processing multiple payments for the same customer over a period of time (for example, if they’re paying you in installments), get a signature for each payment. Clarify on each receipt what that particular payment is for.

- If a customer is being charged a recurring payment, ask for written permission to charge your customer’s card periodically. In the agreement, include the transaction amounts, the frequency of the charges, the length of time the permission is granted, and the cardholder’s signature.

- If you have to provide a refund, always issue it back to the card originally used. If, for some reason, you have to provide the refund through a different method, such as cash or check, get a signed agreement from the customer stating they received the refund.

- Do NOT ask a customer to sign a statement waiving their right to dispute the transaction. If there is a dispute, that signed waiver will hurt your chances of winning.

Receipts

Receipts are a great way to remind your customers of what they bought. They can also provide ways for your customers to contact you if they have any questions or concerns.

- Include your contact information on the receipt – your phone number, address, website, or even your social media pages. If a customer thinks something is wrong and knows how to get in touch with you, they’ll be more likely to contact you instead of filing a dispute with their bank.

- Print your refund or cancellation policy directly on your receipts. This way, your customer’s questions will be answered before picking up the phone or coming back to your store.

- Make sure your name is recognizable. For your customers, nothing is worse than seeing a charge and having no clue where it came from and not being able to figure it out from the receipt.

- Write an accurate description of goods or services sold. This will help jog your customer’s memory and help prevent disputes.

Fraudulent Buyers

Unfortunately, there are fraudulent buyers out there, so look out for these warning signs:

- the buyer places an order through email or by phone to mask their identity;

- they claim to be hearing impaired or in the hospital;

- the buyer places multiple large orders in a short period of time and insists on rush shipping;

- the buyer requests international shipping;

- the buyer’s credit card is declined;

- the buyer inputs the wrong credit card number multiple times;

- the buyer requests an order be split among multiple credit cards;

- the billing and shipping ZIP codes don’t match, and the buyer does not have a reasonable explanation;

- the buyer gives you special instructions, like asking you to pay a third-party vendor for them;

- the buyer orders a large quantity of goods that can be easily resold.

You can help protect yourself from fraudulent buyers by following these best practices:

- Never wire or send money to a third-party at your customer’s request.

- Never use a third-party shipping service you’re not familiar with. Stick with the tried and true, like UPS, FedEx, USPS, and DHL.

- If you’re suspicious, ask your customers for additional information, like a government issued ID.

- Don’t split large orders among multiple credit cards.

Miscellaneous Credit Card Best Practices

There are a few more best practices you can follow to help protect yourself from chargebacks:

- Advertise your products or services as accurately as possible.

- Try to solve any issues with a customer directly, so they don’t file a dispute with their bank.

- Reiterate your return policy.

- Provide exceptional customer service. If you provide exceptional customer service, your customers will be more likely to come to you with any problems, instead of filing a dispute.